Every project has a goal, a timeline, and a budget to manage. However, keeping track of costs, resources, and financial performance can become challenging as projects grow. Project Accounting helps organizations gain a clear view of project finances, ensuring spending stays under control while supporting informed decision-making at every stage.

It is designed to track the financial performance of each project by providing accurate insights into budgets, costs, and resource utilization. In this blog, we will explore What is Project Accounting, how it works, its principles, benefits, and best practices. Read on to discover how it can improve financial control and project success!

What is Project Accounting?

Project Accounting is the practice of tracking and managing the financial performance of individual projects. It focuses on monitoring project revenue, costs, cash flow, and profitability. This allows organizations to compare results against forecasts and make timely adjustments to keep projects on track.

Project Accounting combines both budgeting and cost management to provide a complete view of project finances. Budgeting focuses on forecasting income and expenses, while cost management analyzes how costs affect project performance and overall financial outcomes. Together, these processes help organizations control spending, improve financial visibility, and support project delivery.

Why Project Accounting is Important?

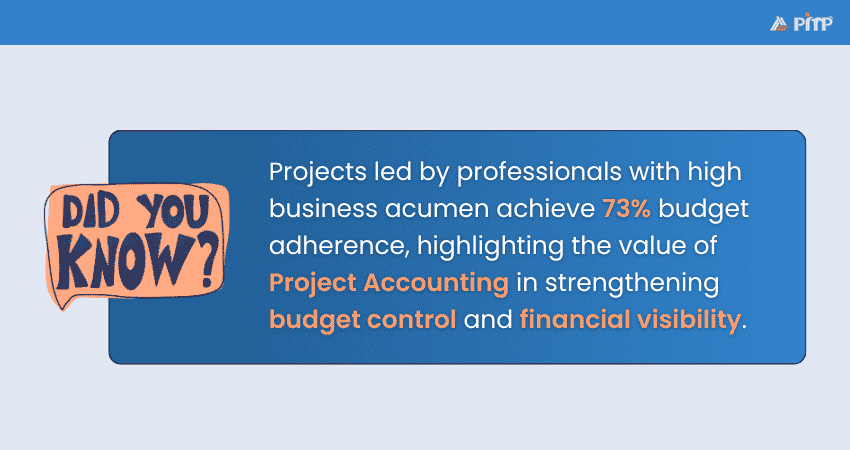

Project Accounting is important because it provides clear visibility into how money is spent throughout a project. By tracking costs across different phases, organizations can allocate resources effectively, manage budgets with greater accuracy, and make informed decisions that support successful project delivery.

It also improves financial forecasting and enables stakeholders to monitor project performance throughout the project lifecycle. In addition, accurate financial records support audits, compliance requirements, and reporting needs, helping organizations maintain transparency and accountability in Project Management.

Steps of Project Accounting Process

The Project Accounting process follows a structured approach that helps organizations plan, track, and manage project finances from start to finish. Let’s look at the steps below:

Step 1: Initiation

The process begins by setting up the project within the accounting system. At this stage, financial objectives, project scope, timelines, cost codes, billing methods, and reporting requirements are defined. Establishing these details early creates a strong financial foundation and ensures all stakeholders work with consistent information.

Step 2: Budget

Once the project is established, a detailed budget is prepared. This includes estimating labor costs, materials, equipment, subcontractor expenses, overheads, and contingency funds. A realistic budget serves as the financial baseline against which actual project performance is measured throughout the project lifecycle.

Step 3: Administration

During the administration phase, financial records and project documentation are managed continuously. Purchase orders, invoices, timesheets, contracts, and expense claims are processed and maintained accurately. Proper administration helps ensure compliance with financial policies while supporting transparent and organized record-keeping.

Step 4: Execution

As the project moves into execution, actual costs and revenue are recorded and monitored in real time. Project Managers compare actual spending against the approved budget, identify cost variances, manage cash flow, and make adjustments where necessary to keep the project financially on track.

Step 5: Maintenance

Financial oversight continues throughout the project by updating budgets, processing contract variations, reviewing forecasts, and managing ongoing financial changes. Regular maintenance ensures accounting records remain accurate and reflect any changes in project scope, timelines, or resource requirements.

Step 6: Analytics and Reports

The final step involves analyzing the project's financial performance and generating reports for stakeholders. Reports typically include budget versus actual costs, profitability, cash flow, resource utilization, and key financial metrics. These insights help evaluate project success, support audits, and provide valuable lessons for improving future projects.

Transform ideas into Agile outcomes and unlock Agile excellence and growth with the PMI-ACP® Certification Training – Sign up now!

Principles of Project Accounting

Project Accounting is guided by a set of principles that help organizations manage project finances accurately and consistently. These principles ensure that costs, revenues, resources, and financial obligations are recorded and monitored effectively. Let’s learn about the principles below:

a) Cost Principle: The Cost Principle states that project costs should be recorded at their original cost when incurred rather than their current market value. This ensures financial records remain accurate, consistent, and verifiable.

b) Matching Principle: The matching principle requires expenses to be recorded in the same period as the activities or revenues they relate to. This provides a clearer picture of project profitability and financial performance.

c) Consolidation Principle: The consolidation principle involves grouping related project activities and financial transactions into a single, consistent framework. This helps create a more accurate view of the project's overall costs and revenues.

d) Full Disclosure Principle: This principle requires all significant financial information and events to be documented and reported. Greater transparency improves accountability and helps stakeholders make informed decisions.

e) Prudence Principle: The prudence principle encourages organizations to use realistic estimates when forecasting project revenues and expenses. This helps reduce financial risk and prevents overly optimistic projections.

f) Liability Principle: The liability principle requires organizations to recognize current and future financial obligations associated with a project. These may include contractual commitments, penalties, or other project-related liabilities.

g) Control Principle: The control principle focuses on implementing procedures and monitoring mechanisms to oversee project finances. Effective controls help ensure accuracy, compliance, and reliable financial reporting.

h) Resource Allocation Principle: This principle ensures that resources are allocated based on project priorities, expected benefits, and financial considerations. Proper resource allocation helps maximize value while maintaining efficient project operations.

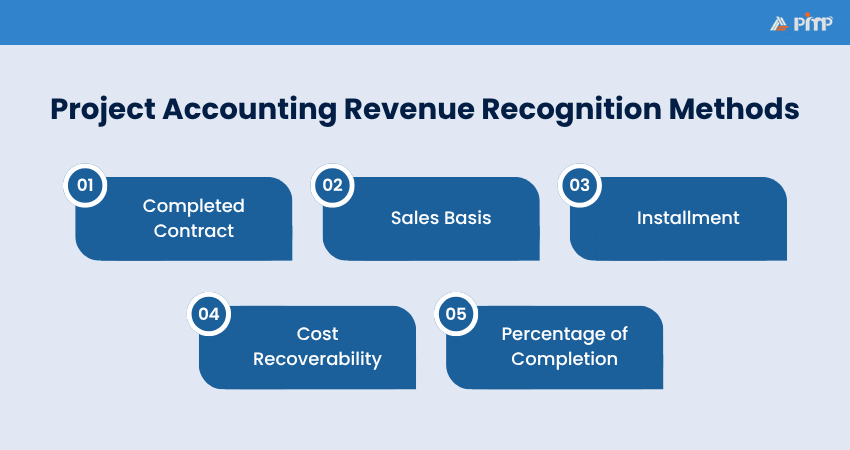

Project Accounting Revenue Recognition Methods

Revenue recognition in Project Accounting determines when and how revenue can be officially recorded after it has been earned. The chosen method depends on the nature of the project, contract terms, payment schedules, and the level of certainty around project completion and costs. Below are some of the revenue recognition methods:

1) Completed Contract

The completed contract method recognizes revenue only after the project has been completed and formally accepted by the client. This approach is commonly used for short-term projects or contracts with uncertain completion timelines. It ensures that revenue is recorded only when all contractual obligations have been met.

2) Sales Basis

Under the sales basis method, revenue is recognized when a sale is completed, and goods or services are delivered. This approach is commonly used for projects with clear and immediate delivery milestones. It provides a straightforward way to record revenue once the delivery process is completed.

3) Installment

The installment method recognizes revenue gradually as payments are received from the client. It is often used for long-term payment arrangements where revenue is collected over an extended period. This method helps align revenue recognition with the actual flow of cash received.

4) Cost Recoverability

The cost recoverability method takes a conservative approach by recognizing revenue only after all project costs have been recovered. It is used when project costs or future revenues cannot be estimated reliably. This helps reduce financial risk when there is uncertainty surrounding project outcomes.

5) Percentage of Completion

The Percentage of Completion recognizes revenue depending on the progress of the project. Revenue is recorded at predefined milestones, allowing organizations to reflect earnings throughout the project rather than waiting until completion. It is particularly useful for large projects that span several months or years.

Develop essential Project Management skills by joining the PMI Project Management Ready® Certification Course today!

Benefits of Project Accounting

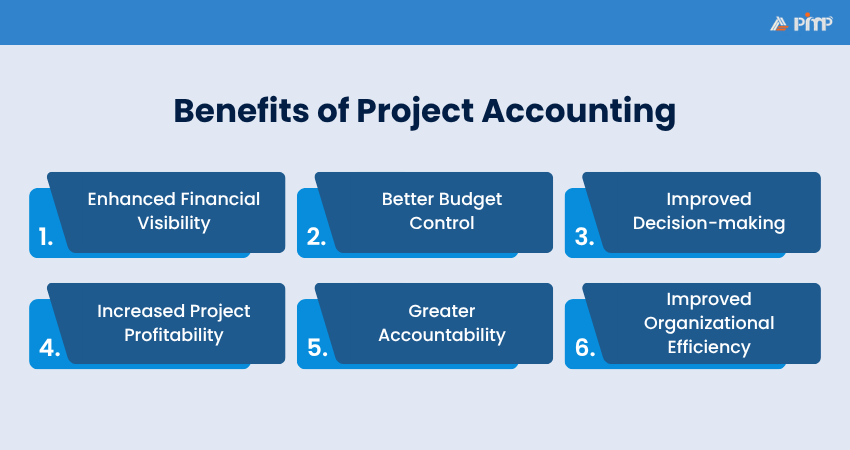

Project Accounting provides several benefits by improving financial management and providing greater control over project performance. Let’s look at some of the key benefits below:

a) Enhanced Financial Visibility: Project Accounting provides real-time insights into project costs, revenue, and profitability. This enables managers and stakeholders to clearly understand the financial health of a project at any stage.

b) Better Budget Control: By continuously monitoring expenses against planned budgets, organizations can identify cost variances early. This helps prevent overspending and keeps projects aligned with financial objectives.

c) Improved Decision-making: Accurate financial data supports informed decision-making throughout the project lifecycle. Project teams can make timely adjustments to resources, schedules, or budgets when required.

d) Increased Project Profitability: Tracking project-specific costs and revenues helps organizations measure profitability more accurately. This allows teams to identify opportunities to improve financial performance and maximize returns.

e) Greater Accountability: Project Accounting maintains clear and accurate records of financial activities and resource usage. This improves transparency and ensures stakeholders remain accountable for project-related spending.

f) Improved Organizational Efficiency: By aligning project financial management with broader business goals, Project Accounting helps organizations use resources effectively. This contributes to better operational performance and long-term strategic success.

Begin your Project Management career with the Certified Associate in Project Management (CAPM) ® Training – Sign up today!

Project Accounting Best Practices and Tips

Project Accounting is most effective when supported by strong controls, accurate documentation, and regular financial reviews. Below are some of the best practices and tips that you can follow:

1) Define Scope and Expectations Early: Clearly defining the project's scope, objectives, and financial expectations from the project initiation helps establish realistic budgets and spending limits. This creates a strong foundation for effective project financial management.

2) Maintain a Detailed Schedule of Values (SOV): A well-structured Schedule of Values breaks down project costs by work category or phase. This makes it easier to track spending and measure financial progress throughout the project.

3) Monitor Cost Reports Frequently: Cost reports provide valuable insight into project spending and financial performance. Consistent monitoring helps identify cost variances and keeps the project aligned with its budget.

4) Manage Requests for Information (RFIs) Promptly: RFIs help resolve missing or unclear information in project documents, contracts, or specifications. Addressing them quickly reduces delays and supports smoother project execution.

5) Establish a Change Order Process: Changes to project scope can significantly affect costs and timelines. Having a clear change order process helps manage modifications efficiently and minimize unexpected disruptions.

6) Track Labor Hours Regularly: Monitoring labor hours against project forecasts helps ensure resources are being used effectively. Regular reviews can also highlight productivity issues and potential budget overruns.

7) Verify Subcontractor Bills: All subcontractor invoices should be reviewed to ensure charges are accurate and approved. This helps prevent unnecessary costs and improves financial accountability.

8) Be Flexible with Budgets: Projects often face unexpected changes or new requirements. Allowing some financial flexibility within the budget helps teams adapt without compromising project objectives.

9) Track Financial Transactions Frequently: Regular tracking of project expenses and revenue provides a clear view of financial performance. This enables faster responses to issues and supports better decision-making.

10) Use Simple and Effective Software: When implementing Project Accounting, user-friendly software can simplify financial tracking and reporting. Starting with straightforward tools helps teams adopt processes more efficiently.

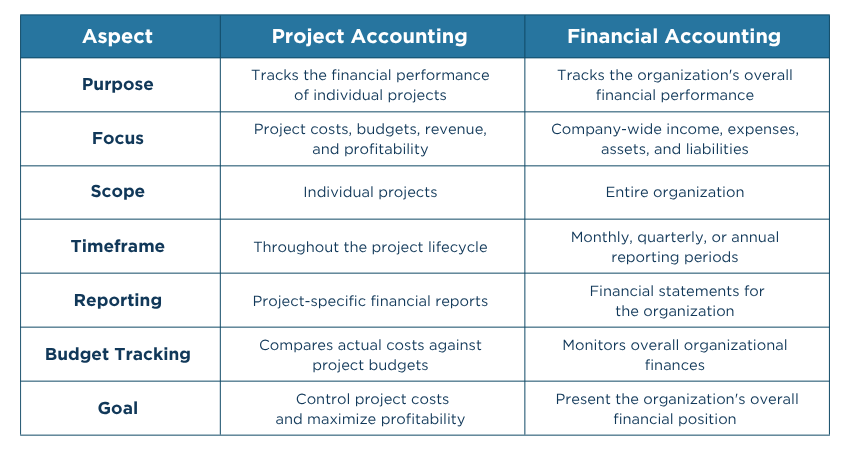

Project Accounting vs Financial Accounting

Project Accounting refers to the financial management of individual projects. It involves tracking project-specific budgets, costs, revenues, and profitability. This provides a detailed insight that helps organizations monitor performance and make informed decisions throughout the project lifecycle.

On the other hand, financial accounting focuses on the overall financial position of an organization. It involves preparing financial statements, recording company-wide transactions, and ensuring compliance with accounting standards. While Project Accounting provides a detailed view of individual project finances, financial accounting offers a broader perspective on the organization's overall financial health. Let's look at their differences in detail with the table below:

Conclusion

Effective financial management is key to successful project delivery, and Project Accounting provides the framework to make it possible. By tracking costs, managing budgets, monitoring profitability, and supporting informed decision-making, it helps organizations maintain control while improving project performance and business outcomes.

Build skills trusted by leading organizations and empower your future with the Project Management Institute (PMI)® Certification Training – Sign up now!

Back

Back

Topics

Topics Courses

Courses

09 Jul 2026

09 Jul 2026

Maria Thompson

Maria Thompson